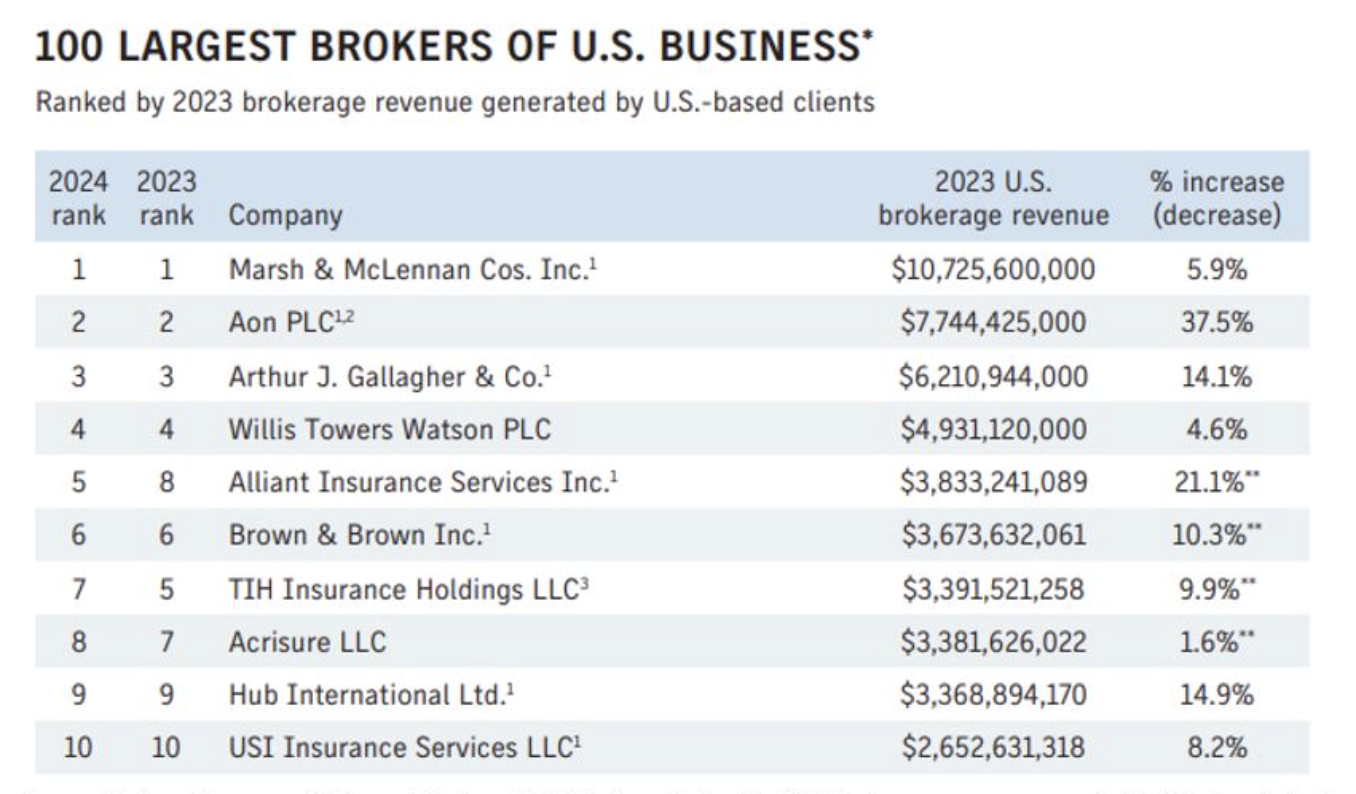

Marsh & McLennan announced plans to acquire McGriff Insurance Services, a provider of insurance brokering and risk management services. The deal is structure as a reverse triangular merger valued at $8.6 billion, according to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of publicly announced transactions.

The transaction includes $7.75 billion in cash consideration, funded by a combination of cash and proceeds from debt financing, as well as Marsh & McLennan’s commitment to assume a deferred tax asset valued at approximately $500 million. Even though Marsh & McLennan is the largest insurance broker in the U.S., the parties do not anticipate regulatory scrutiny and expect to close by year end, though the transaction documents include standard closing condition language that the deal is subject to regulatory clearance.

“Founded in 1886, McGriff specializes in providing commercial property and casualty insurance, surety, employee benefits and personal lines insurance solutions to businesses and individuals across the US,” according to the deal’s press release. “The firm’s coverages include commercial property and casualty, corporate bonding and surety services, cyber, management liability, captives, and alternative risk transfer programs, small business, employee benefits, title insurance, personal lines, and life and health.”

Insurance prices have become a hot button political issue during this election as prices have risen significantly in recent years, across many lines of business: average cost of car insurance soared over 20% from Q2 2023 – Q2 2024, while home insurance rose approximately 11% during just Q1 2023 – Q1 2024. Even as increases moderate, as the following chart shows for commercial lines, those price increases compound over time – not since the great recession have prices decreased significantly.

Commercial Insurance Prices

The US Senate Budget Committee held hearings this past June to investigate “the insurance crisis affecting homeowners nationwide.” Democrats pinned the crisis on increased flooding, hurricanes, and heat waves caused by climate change as forcing insurance providers to either increase rates or drop coverage altogether in order to make covering disaster-prone areas economical. One New York Times study found that insurance providers lost money on homeowners’ insurance in 18 states.

Republicans instead point to government spending and inflation as the primary drivers, even if climatic disasters are a secondary factor. Republican witness EJ Antoni from the Heritage Foundation calculated that “government action, inflation, and regulatory costs account for approximately 90% of the increase in insurance premiums over the past few years,” while Iowa Senator Chuck Grassley cited the “increased costs of labor and materials and the migration to disaster-prone areas as contributing factors.”

With the active and destructive hurricane season of 2024, consumers likely face additional rate hikes ahead.