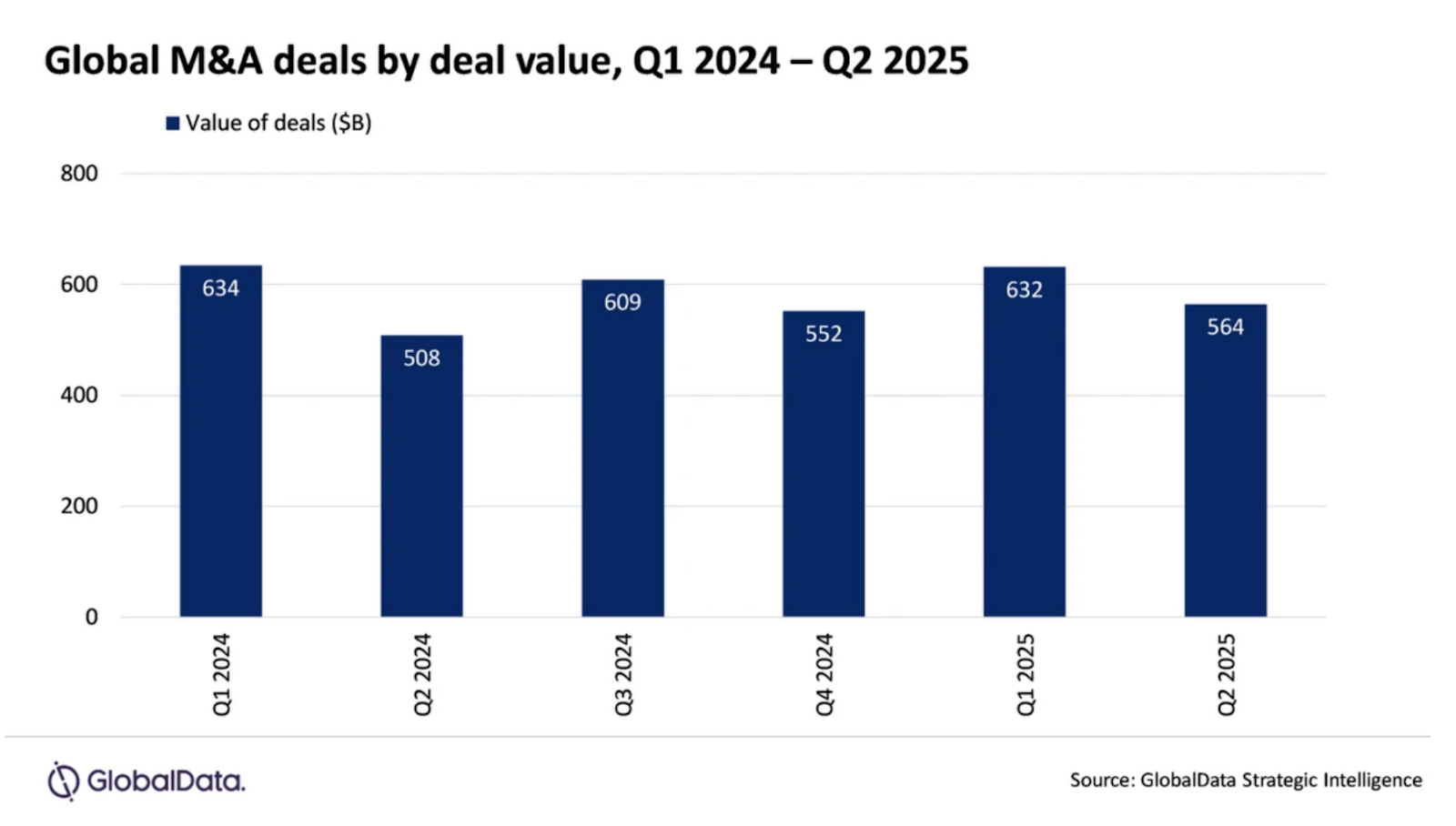

Global M&A rebounded during Q2 2025 with an 11% increase in total deal value year-over-year. Economic growth, declining interest rates, and the resilience of supply chains have fed companies’ appetites for acquisitions.

“Rising geopolitical tensions, changing demographics, increased ESG regulations, ongoing labor shortages, and rapid digital transformation have all intensified the focus on M&A related to supply chains,” according to Priya Toppo at Global Data. “Companies are increasingly prioritizing resilient, localized, and technology-driven supply chains to mitigate risks and improve operational efficiency. This trend is particularly evident in the consumer, industrials, materials, and healthcare sectors.”

There were multiple large deals in the U.S. this quarter that helped propel firms higher in the league table. Flowserve Corporation’s $19.5 billion acquisition of Chart Industries, Inc. announced in June and Fidelity National Information Services, Inc.’s $13.5 billion purchase of Global Payments Inc.’s Issuer Solutions business in April helped lead the pack. Further Blackstone Infrastructure Partners L.P.’s $11.5 billion acquisition of TXNM Energy and Thoma Bravo, L.P.’s $10.55 billion deal with The Boeing Company’s Digital Aviation helped set advising firms apart.

Kirkland returned to the top of the chart this quarter, advising on 7 deals with an aggregate value of nearly $28 billion. They advised both Blackstone Infrastructure in its acquisition as well as Boeing’s Digital Aviation in being acquired. No stranger to the top 5, Latham edged out Cravath for the #2 spot this quarter. While the firm did not advise on any of the largest deals, it’s sheer volume of transactions propelled the firm as it advised on a whooping 11 deals this quarter alone. This contrasts with Cravath, which advised on just 2 deals this quarter – but they were large ones and included advising Flowserve. Winston & Strawn made it back onto the table after a long hiatus by sitting across from Cravath as it advised Chart Industries.

Finally, Skadden did not advise on any of the largest deals this quarter but remained on the leadership table by advising on 5 others.

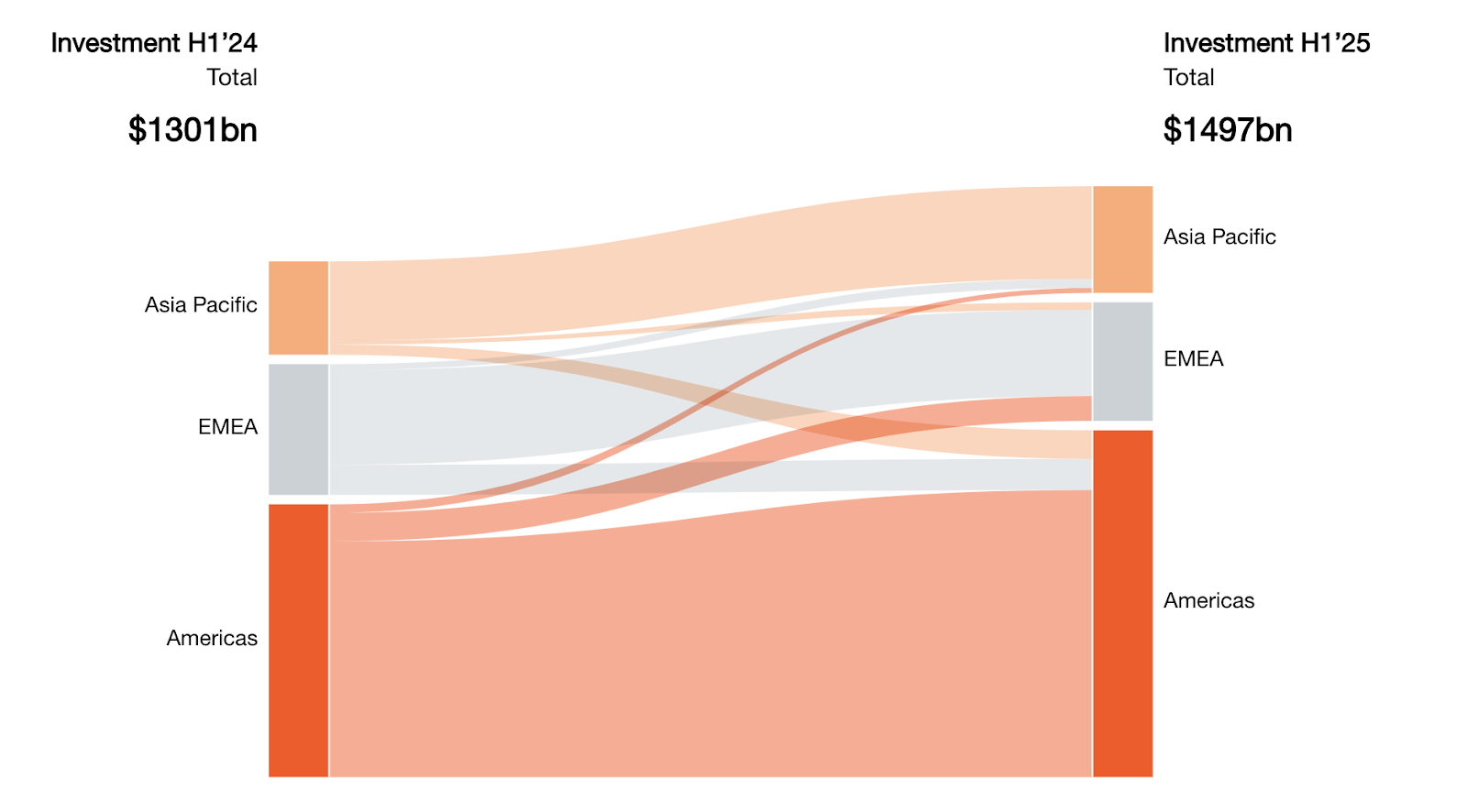

Deal value flows by region from H1’24 to H1’25e

Source: PwC

Despite potential trade wars and continued geopolitical instability, analysts predict more deals ahead. “The deals environment is both frustrating and extraordinarily exciting,” as PwC puts it. “As the market spins new challenges, it’s easy to hoard cash and hit pause, but we advocate doing the opposite: focus on thematics, drive your analysis deeper than ever and bring your strategy to life’. As always, DealPulse will be keeping score.