The federal court system’s Nature of Suit code 850, Securities, covers most litigation related to the stock market. While the largest players in this sector are the Securities and Exchanges Commission and the Commodity Futures Trading Commission, there are notable trends in private litigation. This analysis examines these private lawsuits from January 2019 through August 2023.

Individual Merger and Acquisition Suits

Before 2016, most mergers and acquisitions were challenged in Delaware state court, according to an article in the Vanderbilt Law Review. Many of these cases resulted in disclosure-only settlements in which plaintiffs would drop their cases in exchange for additional disclosures. However, in In re Trulia, Inc. Judge Bouchard ruled against such settlements, stating that the new disclosures were often immaterial. Since then, the bulk of this kind of litigation has shifted to federal courts.

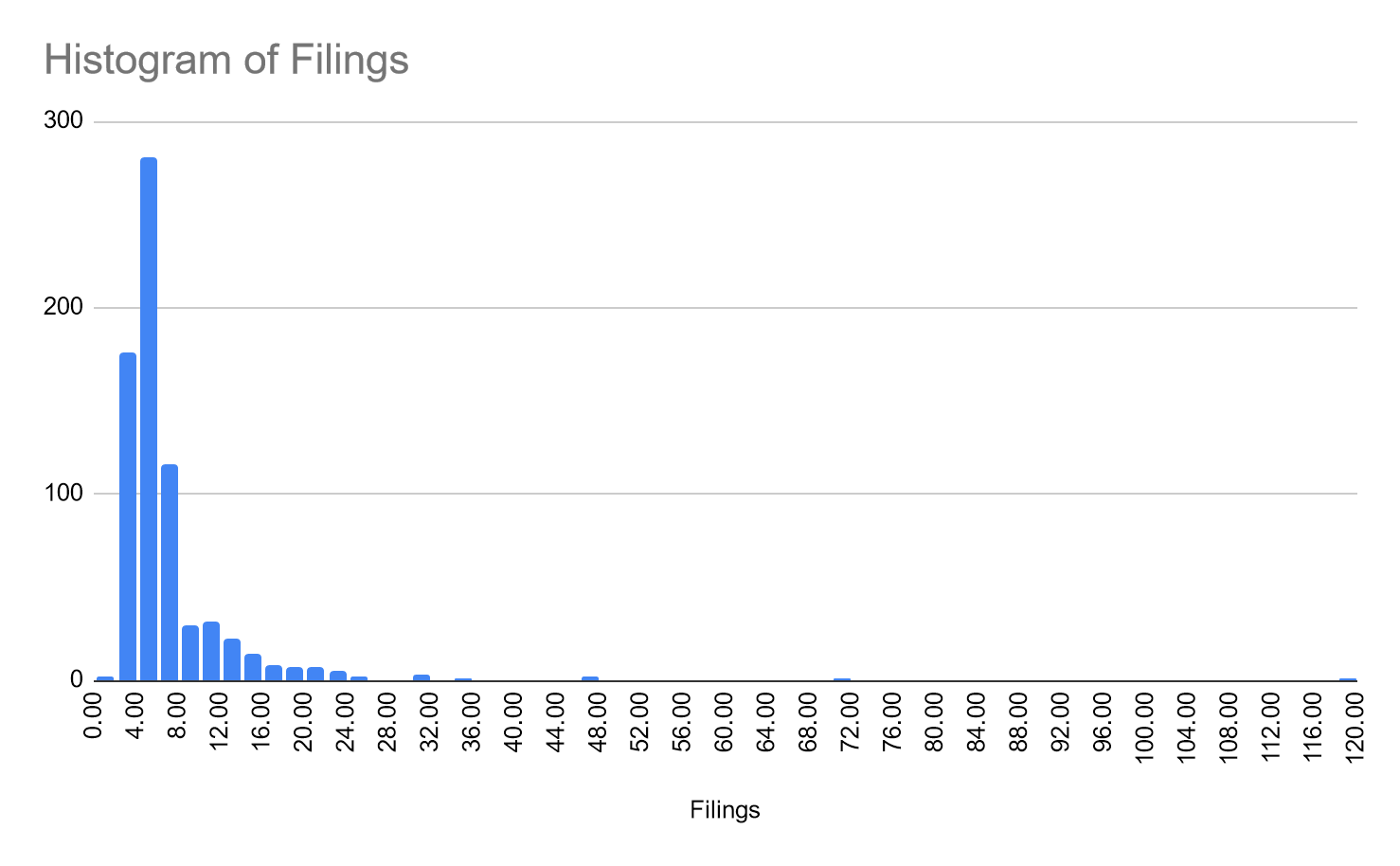

According to Docket Alarm Analytics, the most active plaintiffs in this scene other than federal agencies are Shiva Stein, Stephen Bushansky, Ryan O’Dell, Matthew Whitfield, and Elaine Wang. Taken as a representative sample, their modal case is filed against two publicly owned companies who are merging, lasts one to two months during which five or six filings are made, and concludes with the plaintiff voluntarily dismissing the case.

As reported in the Vanderbilt article, in many cases, the defendants pay the plaintiff’s law firm a mootness fee to cover their expenses in bringing said case; however these fees do not appear in court documents.

While the 1995 Private Securities Litigation Reform Act put limits on how often individuals could serve as the lead plaintiff in securities litigation, these cases skirt this maximum, since they end before the class is certified. The U.S. Chamber of Commerce’s Institute for Legal Reform argues Congress should amend the PSLRA to reign in these, according to them, frivolous suits. The Vanderbilt paper by Thomas, Cain, Fisch, and Solomon, however, argued the Rules of Civil Procedure should be changed to make mootness fees come under judicial discretion.

Overwhelmingly, these cases are filed under the cause 15:78(m) of the United States Code. This section covers the regular disclosures publicly traded companies have to make, including during mergers. A notable minority, however, were filed under 12:22 which covers the disclosures a new company must make upon their formation. These cases were filed exclusively by Matthew Whitfield in the Eastern District of Pennsylvania.

As to the firms representing these serial filers, Shiva Stein and Ryan O’Dell primarily work with Melwani & Chan, Stephen Bushansky with WeissLaw, Elaine Wang with Wolf Haldenstein Adler Freeman & Herz, and Matthew Whitfield fairly equally with Rigrodsky Law and the Grabar Law Office.

Financial Firms

The most commonly charged defendants are J.P. Morgan Securities and Morgan Stanley, followed by Citigroup Global Markets, Goldman Sachs, and Credit Suisse Securities. However, since cases involving the latter three almost always also include the former two, J.P. Morgan Securities’ and Morgan Stanley’s case loads will be taken as a representative sample for most of these analyses.

Typically J.P. Morgan and Morgan Stanley are not the primary target of these cases. Usually they are included as defendants because they underwrote or were otherwise involved in the disclosure documents companies released, and which plaintiffs claim were fraudulent.

Two notable case clusters buck this trend. Between May 1 and July 24th, 2020, J.P. Morgan Securities faced three suits alleging they illegally manipulated, or spoofed, the market for US Treasury bonds and precious metals. These were filed under Section 7:6(b) of the Untied States Code, which concerns foreign transactions by United States persons. J.P. Morgan settled these claims the following October for nearly $1 billion including fines to the US government.

In October 2021 through January 2022, Morgan Stanley faced a flurry of litigation regarding alleged insider trading of a number of Chinese companies. These cases were all filed under US Code 15:78(m), and have yet to be resolved. They are being heard in the Southern District of New York.

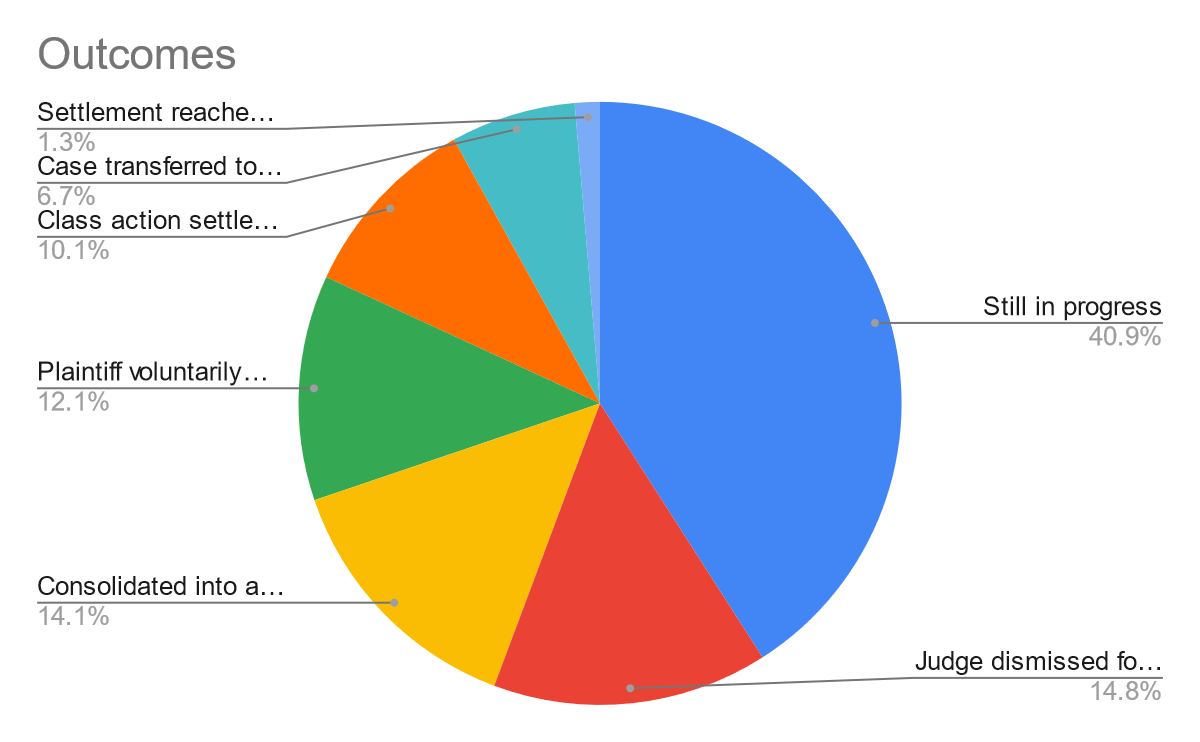

Broadly, unlike the suits covered above, a plurality, 40.9%, have yet to be resolved. Among the remainder, 14.8% were dismissed for failure to state a claim, 14.1% were consolidated into another case, 12.1% were voluntarily dismissed by the plaintiff, and only 10.1% resulted in a class-action settlement. Of the cases that have been resolved, 17% resulted in a settlement.

These cases also last a significantly longer time than those analyzed above. Suits in which J.P Morgan Securities and/or Morgan Stanley were defendants ran a median of 172.5 days and involved 69 filings, while the median suit brought by a serial filer ran 59 days and involved 5 filings. Cases against financial firms were slightly busier with a new filing every 4.5 days compared to a new filing every 5.7 days brought by serial filers, though this could be due to their greater length. These above differences even held when looking only at cases which ended in the plaintiff voluntarily dismissing their case.

The majority of cases against financial firms were filed under 15:77 of the US Code, which covers selling securities under false pretenses. About half that number were filed under 15:78(m) though there are no apparent differences in the content of the cases’ complaints. It could simply be down to lawyer preference.