As private equity firms face pressure to deploy their capital, Thomas H. Lee Partners, L.P. announced that its affiliate will acquire all remaining shares of Agiliti Inc. The deal implies an enterprise value of $2.5 billion and represents a premium of approximately 39% over Agiliti’s 30-day volume weighted average price per share. The parties expect to close during the first half of 2024.

“Agiliti is an essential service provider to the U.S. healthcare industry with solutions that help support a more efficient, safe and sustainable healthcare delivery system,” according to the company’s press release. “Agiliti serves more than 10,000 national, regional and local acute care and alternate site providers across the U.S. For more than eight decades, Agiliti has delivered medical equipment management and service solutions that help healthcare providers….”

While many companies are eager to go public via IPOs or SPAC acquisitions, others like Agiliti are jumping ship to return to private hands. While trading on an exchange as a public company provides liquidity and other benefits, it also exposes companies to a host of regulations, additional financial reporting, and disclosure requirements. “These responsibilities — including remaining in compliance with the provisions of the Sarbanes-Oxley Act (SOX) — can draw management’s attention away from growing the business as executives get caught up in all the details involved in adhering to myriad government regulations,” according to Empower.

Further, public companies are often pressured by their quarterly earnings targets and stock analysts’ scrutiny to prioritize short term profits over longer term gains. Afterall, if management misses a quarterly earning target and the company’s shares plummet, they may lose their jobs before they have the chance for longer term goals that may very well produce larger profits down the road. This drives many public companies to seek to go private – and private equity firms have plenty of cash reserves (aka “dry powder”) to make this happen.

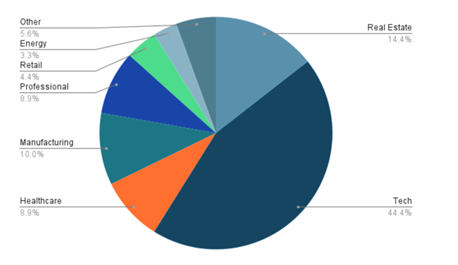

Private Equity Activity by Sector – Q1 2024

According to Hugh MacArthur, chairman of global private equity at Bain, “Record dry powder is stacked and ready for deployment. A sizable chunk of this dry powder is aging and needs to be put to work. Looking into portfolios, nearly half of all global buyout companies have been held for at least four years. In short, the conditions appear to be shifting in favor of hitting the go button.” Private equity firms have focused primary on targets in the technology sector during the first months of 204, followed distantly by real estate and then manufacturing.

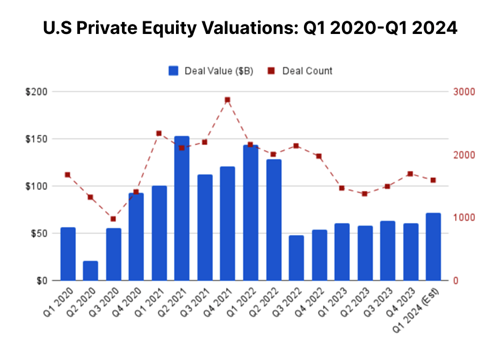

This acquisition arrives as private equity deal activity has slumped from the boom of 2021-2022. After the pandemic lull of 2020, private equity deal volume surged by 35%, setting a record. The low interest rates of 2020 drove many investors to deploy their inexpensive cash in search of higher returns via private equity investments. M&A deal activity dried up drastically during the second half of 2022 and throughout 2023 as high interest rates, violent geopolitical turmoil, and high valuation sent many dealmakers to the sidelines. The fist quarter of 2024 shows a modest uptick in activity that may signal that more private equity firms may be willing to deploy their trove of dry powder.

According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of publicly-announced transactions, Agiliti is advised by law firm Weil, Gotshal & Manges LLP and financial adviser Centerview Partners LLC. Thomas H. Lee Partners is advised by Ropes & Gray LLP and financial adviser Goldman Sachs & Co. LLC.