Allstate Corporation announced a definitive agreement to sell its Employer Voluntary Benefits business to StanCorp Financial Group, Inc., (The Standard) for $2.0 billion. The all-cash deal is structured as an equity purchase whereby Allstate will spin off this Employer Voluntary Benefits segment – with plans to also sell its Individual and Group Health businesses to other acquirers as well.

“Allstate’s Employer Voluntary Benefits business is an industry leader in supplemental and voluntary workplace benefits including Whole Life, Universal Life, Accident, Hospital Indemnity, Cancer and Critical Illness coverage,” according to the deal’s press release. “The Standard, a top group life, disability and ancillary benefit provider, was founded in 1906 and sold its first employee benefits policy in 1951.”

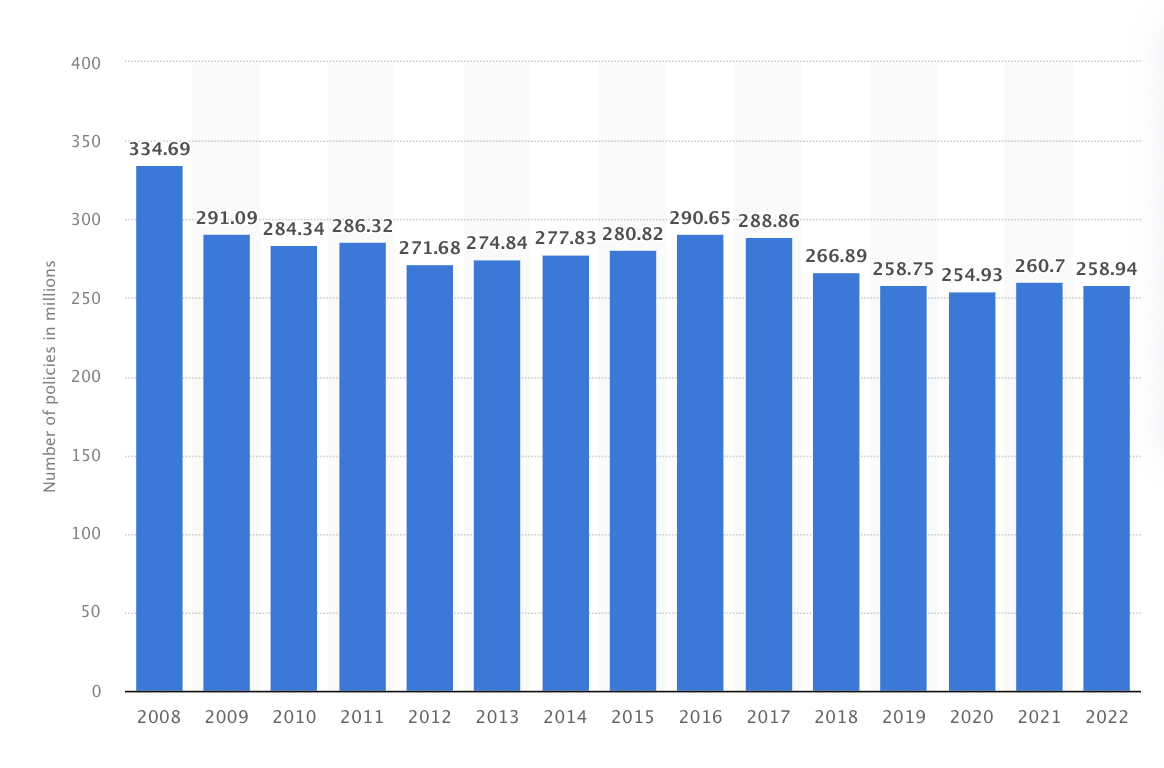

The life/annuity insurance industry is immense, generating revenues in the U.S. alone of over $1 trillion; however, while many purchase life insurance to help support their families if they pass away, U.S. consumers’ interest in life insurance has waned in recent years. While 63% of adults owned life insurance in 2013, that figure had dropped to approximately 50% by 2023. The initial decline coincides with the financial crisis of 2007-2008, when layoffs and job insecurity led many to cut the added expense of life insurance – a trend that has persisted even as the economy improved. In 2008, there were 335 million policies in force, but that figure has dropped by nearly 23% to 259 million in 2022.

Total number of life insurance policies in force in the U.S. 2008-2022

(in millions)

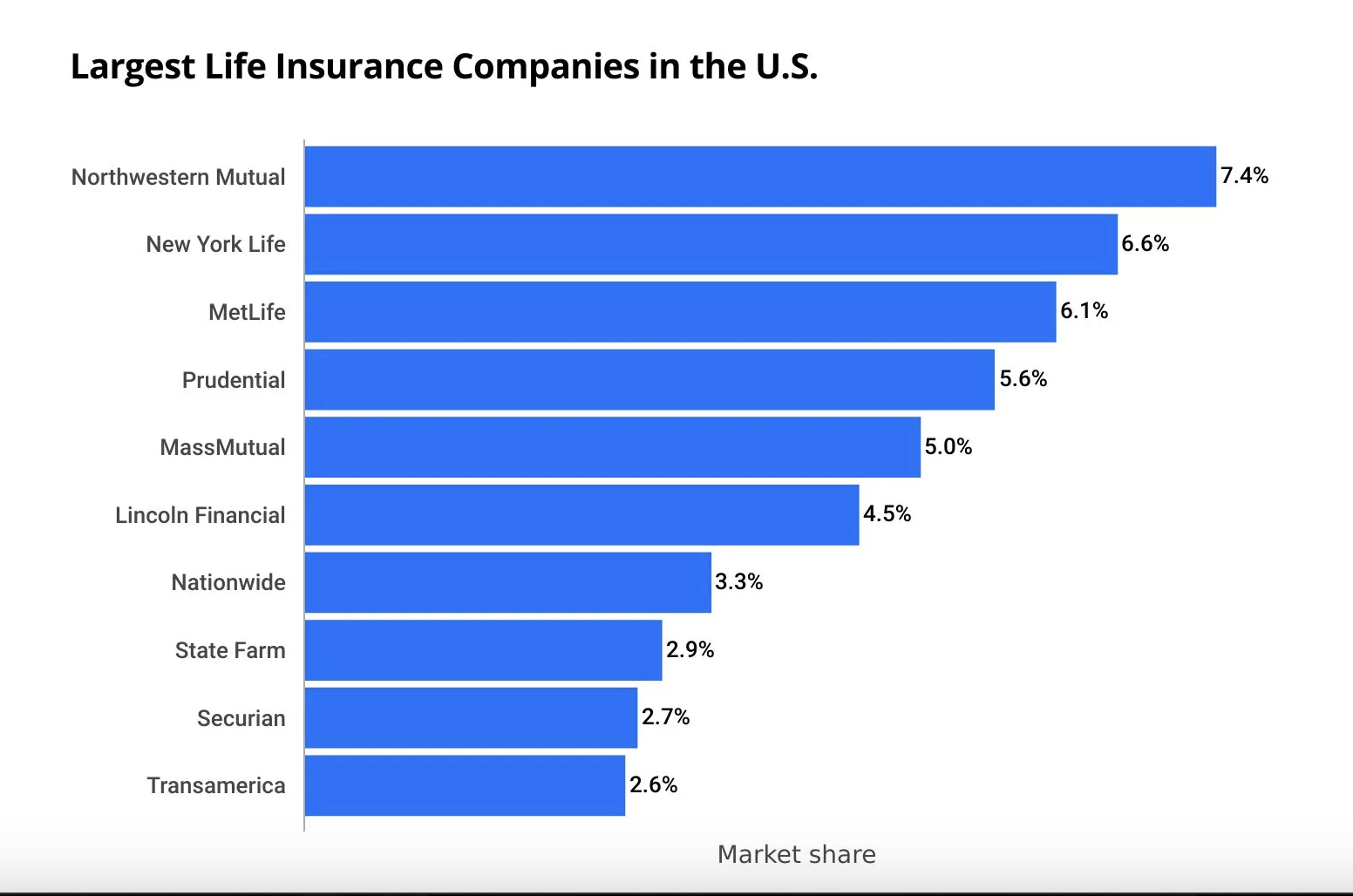

The U.S. is the largest life insurance market in the world, by far. The value of life insurance premiums written in the U.S. is more than twice as large as the next largest market, Japan. Germany, China, and the United Kingdom round out the top 5.

While there are hundreds of life insurance companies in the U.S., approximately 60% of all life insurance is sold by the largest 15 companies. Northwestern Mutual leads the pack with a 7.4% market share, followed closely by New York Life and MetLife.

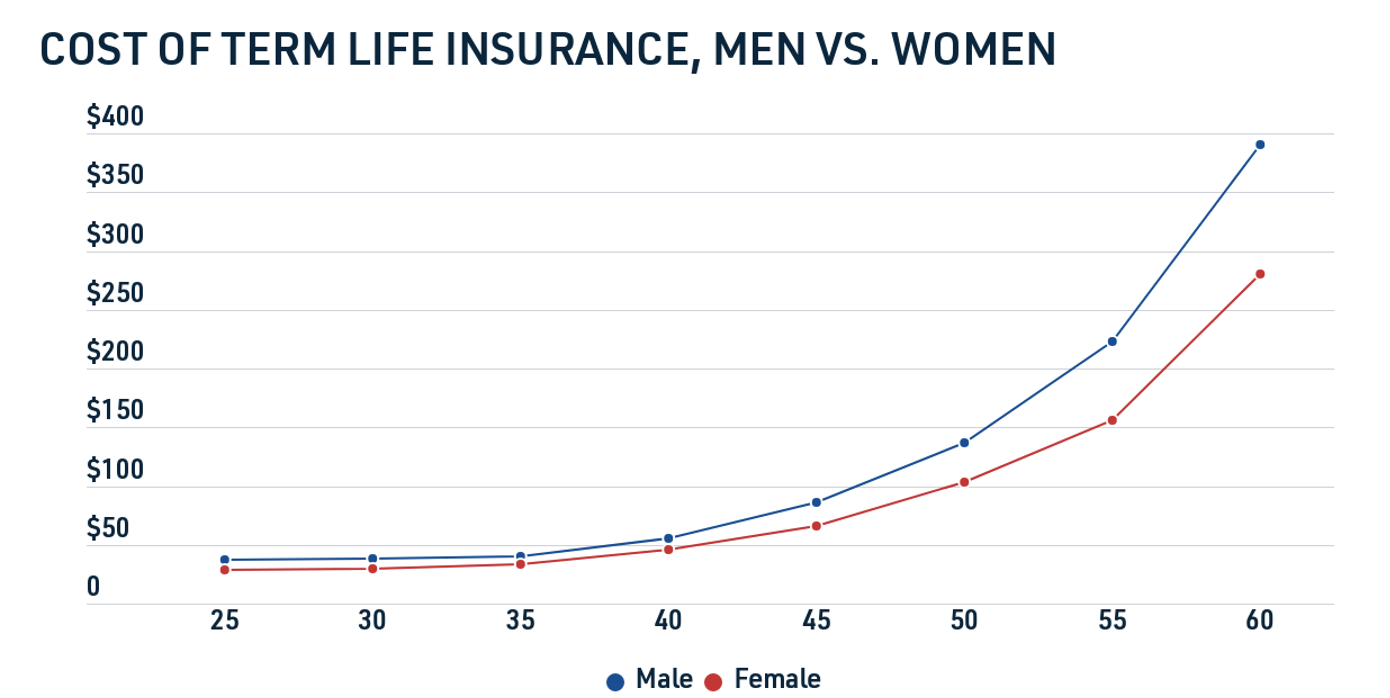

Naturally, life insurance prices fluctuate based on the purchaser. The more likely someone is to die, the higher the premium the life insurance company will charge. Companies often consider whether a person smokes, a doctor’s examination, and other specific health factors. The main determining factors, however, are universal: age and gender. While age seems intuitive, the fact that men are charged more at any age is due to the fact that males are more likely to die than their female counterparts.

Men have higher mortality rates in all age groups. In not one country does male life expectancy exceed women’s. Studies point to a variety of factors to explain this: from estrogen better protecting women from heart disease to behavioral differences where men, in aggregate, take more risks and pursue more dangerous jobs.

According to DealPulse’s M&A database, which harnesses both AI and attorneys to digest the granular deal points of publicly announced transactions, StanCorp Financial is advised by Debevoise & Plimpton LLP. AllState is advised by Willkie Farr & Gallagher LLP.