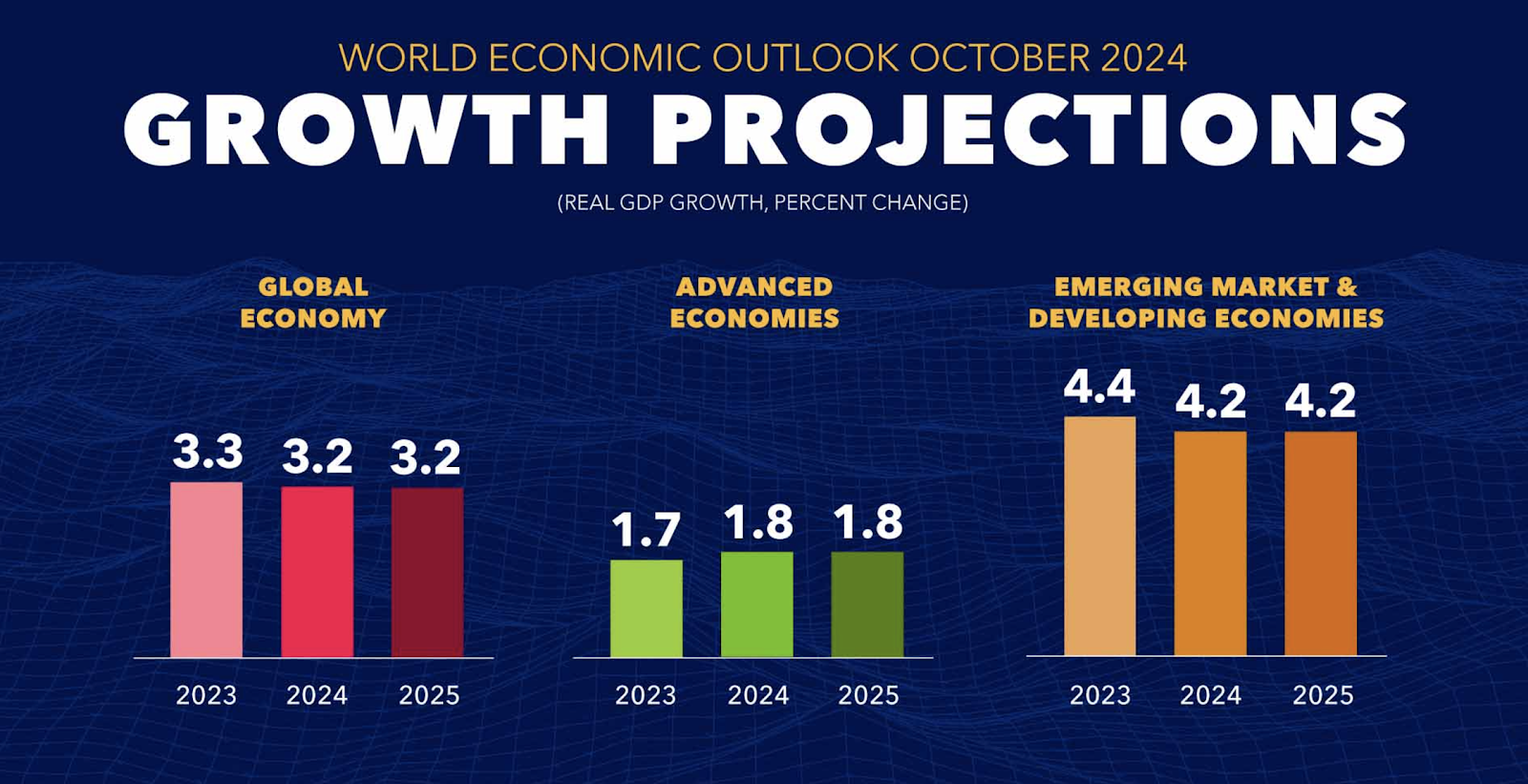

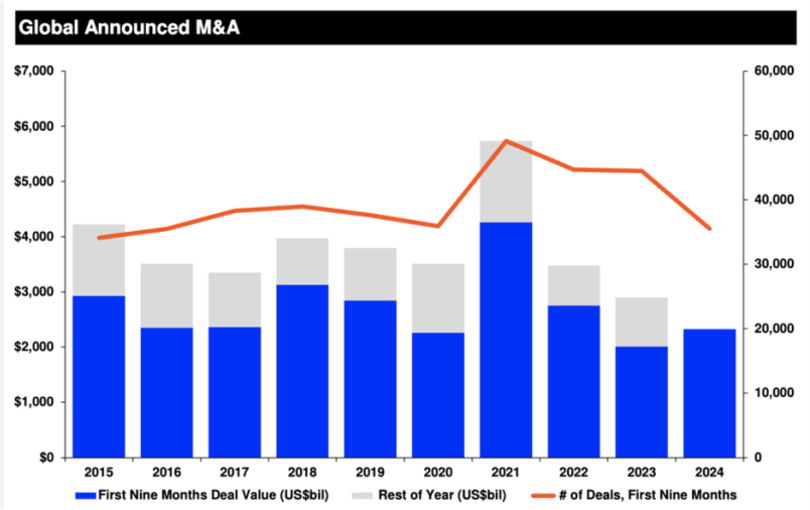

Global M&A clawed its way back from the depths of 2023, as deal values rose modestly to $3.5 trillion despite persistent economic headwinds. The International Monetary Fund projects 3.2% global growth for 2024, a slight decline from 2023’s 3.3% but well below pre-pandemic levels. Persistent inflation and strict monetary policies, coupled with geopolitical unrest, continue to drag on the global economy – and dealmakers’ appetites along with it.

While the global economy is lackluster overall, there are bright spots. The U.S. economy, which is the world’s M&A engine, enjoyed surprisingly robust growth during 2024. Rising at an upwardly revised 2.7%, the U.S. GDP far exceeded other the advanced economies’ overall growth of 1.8%. With surprising strength in the U.S., we saw an increase in the combined value of M&A transactions, even if the volume of deals dropped.

Source: International Monetary Fund

DealPulse’s M&A database tracks publicly-announced U.S. deals over $25 million in value, harnessing both AI and attorneys to digest the granular deal points of each transaction to allow for comparisons across industries, specific deal terms, and both legal and financial advisors. This analysis focuses on deals announced during the calendar year.

Source: IFLR

While Healthcare had led the way in 2023, this year, Novo Holdings’ $16.5 billion acquisition of Catalent did not even break the top 3 deals of 2024, because it was dwarfed by transactions in financial institutions and technology. Capital One’s $35.3 billion deal to acquire Discover led the pack. Announced in February, the deal faced intense regulatory scrutiny as the 4th largest credit card company sought to acquire the 6th largest to create a giant trailing only Chase and American Express. The deal surmounted a key hurdle last month as the Office of the Delaware State Bank Commissioner approved the merger.

In second place, Semiconductor giant Synopsys announced its $35 billion acquisition of software maker Ansys, Inc. last January. This deal has likewise faced regulatory scrutiny, with pushback from the U.K. Competition and Markets Authority, but the companies expect to close the deal in 2025.

Rounding out the top 3 is the union of snacking giants Mars, Incorporated and Kellanova. Announced in August, the $34.9 billion merger will bring iconic brands M&Ms and Snickers together under the same umbrella as Pringles and Pop-Tarts. While prices at the grocery store have become a hot-button political issue, the parties do not anticipate fierce opposition from regulators.

While some analysts had high hopes for a strong resurgence in M&A during 2024, this column as more measured in its outlook for the year, predicting more modestly that these last 12 months would top the lows of 2023 while remaining a far cry from the boom of 2021. For 2025, we can expect M&A activity to gain momentum as interest rates moderate further and the Trump Administration adopts less hawkish anti-trust policies. Either way, we can expect more blockbuster deals to come in 2025.