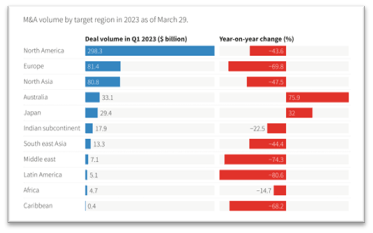

Global M&A volume plummeted during Q1 2023 as rapidly increasing interest rates, geopolitical turmoil, recession fears, and now the unfolding banking crisis have all dampened companies’ appetites for acquisitions. Deal volume in the U.S. dropped 43.6% vs. the same period last year – but many relatively smaller deals were announced. Matterhorn’s M&A database tracks publicly-announced US deals over $25 million in value, harnessing both AI and attorneys to digest the granular deal points of each transaction to allow for comparisons across industries, specific deal terms, and both legal and financial advisors.

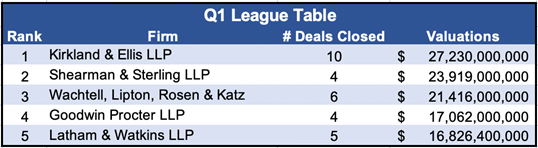

UBS’s forced union with ailing Credit Suisse topped headlines as the Swiss averted a potential catastrophe; but as far as deals announced under U.S. law, Silver Lake’s acquisition of software giant Qualtrics for $12.5 billion led the pack. Four firms advised on the acquisition and it catapulted into the top 5 firms league table for the first time Shearman & Sterling LLP.

Kirkland & Ellis, a frequent member of the top 5, topped the charts this quarter. Advising on a whooping 10 deals, Kirkland was propelled primarily by its advising Oak Street Health in its acquisition by CVS. In addition to advising Qualtrics, Shearman & Sterling sat opposite Kirkland on the CVS/Oak Street deal, helping the firm to land the #2 spot.

Another usual face on the list, Wachtell landed at the third spot as it advised on 6 deals announced during the quarter. Goodwin Proctor achieved the fourth spot by advising on 4 large deals, narrowly beating Latham Watkins, which came in at fifth place this quarter.

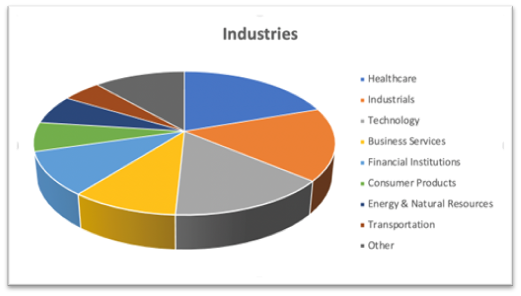

Analyzing the industry breakdown of deals this quarter, it is especially noteworthy that industrials have shot up to the second spot, trailing only healthcare, which leads the chart most quarters. Technology climbed back to the #3 spot after falling to the 4th last quarter.

Analysts expect increased volume ahead as investors take advantage of depressed valuations. According to Reuters, “The depressed market valuations also presented an opportunity for prominent activist investors to launch new proxy fights, with dealmakers anticipating a boost to M&A volumes from activist campaigns in the coming quarters.”